There’s a new top dog in golf and, for the first time in a long time, it’s not Acushnet.

Or maybe it still is. It depends on how you keep score.

Acushnet’s 2019 financial report hit the streets last week. Top-line sales for Titleist, FootJoy and all its associated brands total $1.68 billion for the year, a very Acushnet-like 2.9-per-cent increase (nearly $48 million). However, Acushnet now is looking up at a competitor as earlier this month Callaway reported 2019 sales totaling $1.7 billion.

We knew it would be close but, as they say, if you’re not the lead dog, the view never changes.

There is a but, however.

The Bottom Line

Businesses exist to make money – no news flash there – and in that sense, Acushnet still is the lead dog. The company is reporting a 2019 net income (profit) of $121 million. That’s a 21-per-cent increase over 2018 and if you like to keep track of these things, a leap and a bound ahead of Callaway’s reported net income of $79 million.

As with Callaway’s financials, headlines are sexy, but the devil is in the details. We certainly don’t claim to be financial analysts or advisers but we can read. Whereas Callaway experienced unprecedented sales growth in 2019, it also had new capital expenditures – presumably for the Chicopee ball plant – that dragged net income down from the previous year. Acushnet’s net income increase was fueled by a $47.7-million sales increase combined with relative cost controls and a $7 million lower income tax burden.

Acushnet did have a couple of acquisitions that helped the bottom line to varying degrees. In Q4 2018, it purchased the Sugar Land, TX-based PG Golf, the world’s largest wholesaler of recycled and refinished golf balls. Its brands include Reload, which is sold worldwide, and Hunter, which is sold exclusively through Walmart.

In July, Acushnet purchased KJUS, a Swiss-based maker of high-end ski and golf apparel. The report cites a full year of PG Golf income as being partly responsible for a nearly $28-million increase in 2019 ball sales. Since KJUS was added midway through the year, financial results weren’t broken down into specifics. The report does say KJUS did benefit sales in Europe, however.

Breakdowns

Does a mere 2.9-per-cent increase in sales surprise you? It shouldn’t. Since 2016, Acushnet’s annual sales increases have ranged from three to seven per cent while net income has jumped from $45 million on sales of $1.57 billion in 2016 to $121 million on $1.68 billion in sales last year. Quarterly, Acushnet missed sales projections in the first two quarters of the year but had a boffo Q4 which led to a surge in stock prices.

The product category breakdown tells an interesting story. As you’d expect, the golf ball sales are otherworldly silly. Fueled by the new ProVs released in Q1, ball sales topped $551 million in 2019, an increase of $27.6 million and 5.3 per cent over 2018. By comparison, Callaway sold $211 million worth of balls last year.

Balls are clearly Numero Uno at Acushnet.

Titleist clubs, however, had a down year with global sales dropping 2.4 per cent and nearly $11 million. Total club sales topped $434 million, but a deeper dive shows club sales up by nearly $8 million in the U.S. While not broken down by product category, overall sales in Japan and what Acushnet identifies as Rest of World (everything that’s not the U.S., Europe, Japan or Korea) were down eight per cent and 4.5 per cent respectively. Specifically, while Titleist released the new T-Series irons and hybrids in 2019, Vokey wedges and the TS drivers and fairways were in the second year of their cycle, which no doubt had an effect.

European sales numbers rose by nearly five per cent and almost $11 million, largely due to the KJUS acquisition and increased ball sales.

FootJoy sales rose a modest 0.5 per cent from $440 million to $442 million, largely due to higher selling prices on non-shoe products. The average selling price for shoes was actually lower in 2019. Titleist gear – hats, bags, gloves and other branded knickknacks – also rose modestly at 2.7 per cent (up nearly $4 million). Overall gear sales totaled $150 million.

As mentioned earlier, Japan is a problem spot for Acushnet. That eight-per-cent decrease in sales ($16 million) is largely attributed to declines in clubs and FootJoy.

Other Tidbits

Again, the fun in these reports is in the details.

For those of you scoring at home, Acushnet spent $51.6 million dollars on R&D last year, or three per cent of sales which is the industry standard (Callaway spent an even $50 million). Selling, general and administrative expenses, which include salaries, marketing and overhead not related to actually making product, totaled nearly $628 million.

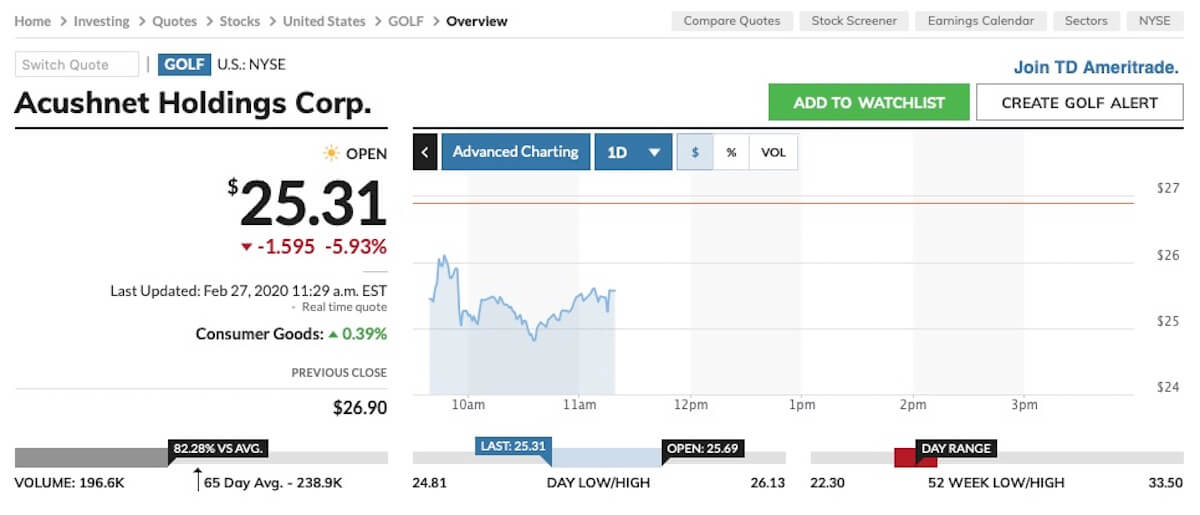

Acushnet’s stock (GOLF on the NYSE) went on a bit of a roller coaster ride Thursday when the report was released. It opened at $25.69 per share and within a half an hour bottomed out at $24,81. By close Thursday it was $25.59 and by close Friday it was back down to $24.90. How much of that is due to the financial report and how much was due to the tank job the market took Thursday and Friday is an open question, but Acushnet stock has been trending downward for the past month. It was at nearly $32 per share Jan. 30 and was over $30 just a week-and-a-half ago. This time last year, Acushnet stock was worth $24.90 per share.

For what it’s worth, Acushnet stock dropped after last year’s report as well. Also for what it’s worth, Callaway stock prices have dropped since releasing its financial report earlier this month.

Again, we are not financial advisers or stock market experts. We just like to read.

2020 Outlook

In Acushnet’s press release, CEO David Maher sounds bullish on 2020, as you’d expect. As head of a publicly traded company, that’s one of his most important jobs.

“We have a number of exciting new initiatives in place across all product categories. We’re committed to sustaining our Pro V1 momentum and launching new AVX, Tour Soft and Velocity models. We are poised to launch new Vokey SM8 wedges and Cameron Special Select Putters in the first quarter and new Titleist metals later in the year. We also look forward to several new Titleist gear and FootJoy products and the continued growth and development of KJUS.” – David Maher, Titleist CEO

Lurking, however, is the coronavirus. The report estimates a $40-million negative impact attributable to the virus in 2020, on projected sales for the year of $1.7 billion.

In the big picture, the horse race between Callaway and Acushnet means different things to different people. Callaway has finally caught and passed the lead dog in overall sales which, for any competitive person, is a satisfying achievement. However, the name of the game is profit and in that respect, Acushnet remains king.

But the financials tell us we have two very different companies with different dynamics. Callaway has been and, in all likelihood still is, in acquisition mode as it diversifies itself. It’s basically equipment-proofing its business. Acushnet, by design and temperament, is a much more conservative company but it appears to be doing the same thing.

Acushnet’s ball business is so strong that it has reached annuity status and FootJoy, despite relatively modest growth over the last two years, is also a consistent money-maker. The July acquisition of KJUS for $28.7 million (compared to the $476 million Callaway paid for Jack Wolfskin) is smart strategy. KJUS adds a high-end (and presumably high-margin) apparel brand to both the U.S. and European markets, another layer of diversification.

As we mentioned in our look at Callaway’s 2019 financials, the golf company of tomorrow may not, in fact, be a golf company at all. Instead, Callaway and, to a lesser extent, Acushnet are morphing into lifestyle companies that happen to sell a lot of golf clubs and golf balls.

THOMAS

4 years ago

Interesting, as all converge on price, volume, and performance. The future could quite possibly be a Flat Line. Thus it will be personnel perceived perfomance and number of pros playing ie: Prov!