Five years ago everything at Callaway Golf changed. Chip Brewer signed on as CEO, and shortly thereafter former TaylorMade guy, Harry Arnett, was hired to repair Callaway’s broken marketing machine. Arnett’s first act of meaningful business was to declare a 5 Year War on the practices that had caused the once vigorous Callaway to become stale, mundane and completely distracted by what it was doing instead of being focused on who it was doing it for.

While Harry’s War was a rallying call for change within the company, the battles have spilled over into the larger industry. One by one Callaway is bringing the fight to its competitors, and it’s winning with an entirely different and uniquely modern (for the golf industry, anyway) strategy. Five years after Arnett’s declaration, the company remains focused on the Callaway Way, and that means it’s focused on the consumer.

Call it the Carlsbad Trojan Horse.

Whatever the impetus and regardless of how it all went down, it’s 2017 and Callaway is primed to become the undisputed leader of the golf equipment world… and that assumes it isn’t already.

The BREW-PRINT for Success

It all starts with Chip Brewer, CEO and resident mastermind. He sets the strategic vision which, in a macro sense, is one that emphasizes in-house innovation and performance.

That said, Brewer has shown a willingness to seek out opportunities to expand Callaway’s reach. Callaway’s investment in TopGolf has paid literal dividends, and the recent acquisition of OGIO suggests Brewer isn’t afraid to reach outside of its industry. Sure, OGIO makes golf bags and golf apparel, but golf is only part of the OGIO catalog.

Brewer isn’t afraid to cut either. The sale of the Top-Flight and Ben Hogan brands shortly after his arrival are your cases in point. Trimming the fat allowed Callaway to grow its core hard goods business by managing costs, expanding the global footprint, and pushing engineers to create proprietary technologies which hopefully translates into increased market share and returns for investors. That’s balance rivaled only by Cirque de Soleil.

Callaway’s A-Team features Harry Arnett (Senior VP of Marketing), Chad Coleman (Social Media Director), and Dr. Alan Hocknell (Senior VP of R&D), and near-countless others whose names aren’t familiar to Callaway’s Internet base. Each individual is uniquely gifted in his respective position, but ultimately, it’s the combined efforts of the entire team that has transformed Callaway into the first truly modern golf company.

We’ll get to that in a bit.

None of this happened by accident. The higher-ups might say it’s all the result of sticking to a single focus and doing “what we do well”, but that’s an oversimplification. Every member of the team appears keenly aware of what’s happening in the market and how their Carlsbad neighbors are faring. Meanwhile, Callaway is constantly assessing its own strengths relative to those of its competitors – all in an effort to take Callaway to the top of the mountain.

Every button pushed is strategic. Every move is calculated. How do you dominate the landscape? One golfer at a time.

CATEGORY PLEASE

Chip Brewer attributes the mostly positive 2016 financial report to “well-rounded performance across all categories.” Those are broad strokes, but a more detailed look at each equipment category offers a better explanation of what he means.

Metalwoods

Even if the sum total of the numbers argue the case, it’s hard to call yourself the #1 Company in Golf if you’re not winning with the most visible club in the bag. Drivers still move the needle and chicks still dig the long ball.

For the last decade and a half, retail sales within the category have been dominated (with minimal interruption) by Callaway’s most visible competitor, TaylorMade. Callaway has spent the last several years chipping away at TaylorMade’s lead and it’s bullish on the idea that 2017 will be the year it lays claim to the title of #1 Driver in Golf. It finished January number one in the category. Not to be taken lightly – we’re talking about consumer sales, not Tour usage where, unlike retail, it’s the manufacturers that pay for the privilege of having professionals play their gear.

If Callaway keeps the lead, and I believe it will, EPIC and its Jailbreak technology will be the product that thrust Callaway past the tipping point.

Arnett predicts “every driver going forward will have to be made like this or it’ll be obsolete.”

If you find yourself a little skeptical and feeling like you’ve heard this type of rhetoric before, you have. Mark King (then CEO of Arnett’s previous employer) touted the 2012 RocketBladez irons as “the biggest iron innovation to date.” According to King at the time, iron slot-technology was a game-changer. He cautioned, “If your iron doesn’t have a speed-pocket, it’s outdated.” History has thus far proven King wrong and that’s the thing about history – it doesn’t care who you are.

Jailbreak may be every bit the pioneering technology Callaway claims it is. It could also prove to be nothing more than the technology de jour; outdated, obsolete, and overhauled by 2018.

Within this context, EPIC is more than a name. EPIC(ly) is how this line must perform if it truly is to become the benchmark by which other OEM’s are judged. Time, testing, and consumer perception will determine the new reality.

Trickle Down

The ancillary benefit of a juggernaut flagship driver is that its impact trickles down the line into the fairway woods and hybrids. Sell one and a fair amount of the time you sell 2 or 3, or more. As the driver goes, so will the Epic fairway and hybrid. And that’s exactly why Callaway believes it’s more than just the driver category in play. When the dust settles, will Callaway disrupt TaylorMade’s more than decade-long reign as the #1 Metalwoods Company in Golf (based on retail sales)? Harry Arnett is confident it’s going to happen.

Irons

Callaway already holds the #1 position in the US (22.6% which is up 1.5% from a year ago). The 22.2% market share in Europe is the highest it has ever been for Callaway and they’re now the #1 brand on the continent.

This is only happens when your entire lineup is solid. To be #1 you don’t get to have a weakest link. Though less publicized than the driver, a solid iron line up is vitally important for Callaway to maintain and extend its market share and keep its resume complete. The company offers high-performing irons in every sub-category, and with a ceiling price of $1,200, there’s still some value within the range for consumers.

Wedges

The Mt. Rushmore of wedge design doesn’t have many faces carved into it, but Roger Cleveland’s is unquestionably one. While some may not be aware, for the last 21 years, Cleveland has been on team Callaway.

His reputation speaks for itself, but perhaps the greatest compliment comes by way of his former company’s (Cleveland Golf) efforts to keep his name off Callaway wedges. The last time Cleveland’s name appeared on a Callaway wedge, Cleveland sued him (well, Callaway technically).

When you’re good, people remember you. When you’re an icon, they litigate.

Callaway wedges are currently #2 on the PGA Tour, #1 on the LPGA, and a strong #3 in retail sales. Titleist’s Vokey brand maintains a sizeable lead, particularly in the retail category, but Callaway is proving you don’t have to win every battle to win the war.

Putters

Given only a cursory glance, the recent acquisition of renowned putter artisan David Mills (TP Mills) may seem awkward. Callaway’s Odyssey brand is #1 in a variety of categories (worldwide sales and PGA Tour usage to name two), and the addition of former TaylorMade VP Sean Toulon’s company, Toulon Design, seemed to fill whatever custom-milled-bespoke niche Callaway felt it needed to fill.

While Sean Toulon may be every bit a putter designer, his 30 years of industry experience is his real capital. His putters are nice looking and perform well. They will certainly sell, but Toulon can’t do what Mills can – and that’s go directly after the absolute king of the hand-crafted, custom, putter as a piece of art world – Scotty Cameron. Mills has pedigree, experience and an established reputation as a world-class putter maker. Mills doesn’t need to do anything contrived to compete in his space, and that’s right in line with Brewer’s philosophy.

While Callaway and Mills are still finalizing details, expect to see some significant information no later than end of 2nd quarter.

Golf Balls

Callaway has the #1 selling ball at non-green grass accounts and is #2 overall within the category. In the fall of 2016 it had a 15% market share worldwide and this didn’t include whatever amount they claimed from the departure of Nike, who then controlled a little over 5% of the ball market.

Speaking of Nike, Callaway poached former Nike ball designer, Rock Ishii, who headed up the company’s ball department and worked with staffers including Rory McIlroy and, of course, Tiger Woods. We don’t yet know what that means for the Callaway ball franchise, but it’s worth noting that Ishii has a history of pushing boundaries.

The backdrop here is important. Titleist has plenty of company in the tour ball category, and some of its competitors charge considerably less for their products. Consumers are starting to realize they don’t need to pay $48/dozen for premium performance. Callaway, TaylorMade, Srixon, Snell and Vice all make balls which perform equally as well for many golfers, and in some cases, they cost significantly less. Both the Callaway Chrome Soft series and new Srixon Z-Star series retail for $39.99/dozen. Vice sells for $35 a dozen and Snell, at $30/dozen, come in a bit lower still.

Attempting to undercut Titleist on price was previously a recipe for failure. That’s because consumers associated the premium price with better performance. With the growing popularity of the Chrome Soft, Snell’s My Tour Ball and Costco’s Kirkland Signature, the myth that premium performance mandates a premium price has been debunked, and that has created new opportunities in the ball market for both brands and consumers.

MACRO ECON 101

It’s important to separate Callaway the golf company from Callaway the portfolio investment. Callaway, as a golf company, has everything it needs to assume the title of Undisputed #1 Company in golf. It has the product and it sure as hell knows how to execute a marketing plan. That isn’t to say there aren’t improvements to be made. One of Brewer’s gifts is acquiring contributory resources which help support the overarching framework or what Brewer terms “structural advantages driven by momentum” which have “proven operating ability and strong capital structure.”

Brewer’s strategy makes a lot of sense if you’re trying to sustain and carefully advance your position as the leading golf company in the world. You focus on your core business, invest heavily in R&D, and strategically acquire people like Sean Toulon, Rock Ishii and David Mills. When other companies exit the space (Nike, Ben Hogan) or get sold off (TaylorMade?), you’re waiting and ready to capture additional market share.

The First Modern Golf Company

Callaway’s marketing strategy is diametrically differently than that of any of its direct competitors. Making golf relevant to millennials and outsiders through associations with Red Bull (Callaway Distance Lab) and the Geto Boys’ Scarface (aka Brad Jordan) is a play other OEMs are reticent to make. Promotions like these and others (Callaway twice turned Petco Park into a golf course) fly in the face of convention while disrupting any notion that golf’s traditions are the exclusive domain of the khaki-clad, country club elite.

To stand above the noise, you have to take some risks. At the heart of this modern approach is what Callaway is doing with self-produced content like Arnett’s quasi-talk show, “Callaway Live”, Callaway’s “The Pirate Ship Show” podcast, and other newsy tidbits located under the News+Media tab on the Callaway website.

At face value, it may not seem like much of a paradigm shift, but the larger story is in how Callaway has taken complete ownership of its message. Rather than exporting the Callaway brand to outsiders to develop and broadcast content, they’re doing it in-house. The concept of Community Branding has positioned Callaway as the primary source for Callaway news. Don’t be surprised when you see other OEMs attempting to mimic Callaway’s approach to proprietary branding, though that may take some time.

As MyGolfSpy’s Tony Covey observes, “Callaway is producing content while its competitors are still making ads.”

But none of this necessarily means Callaway is a good investment.

HUH? WHY NOT?

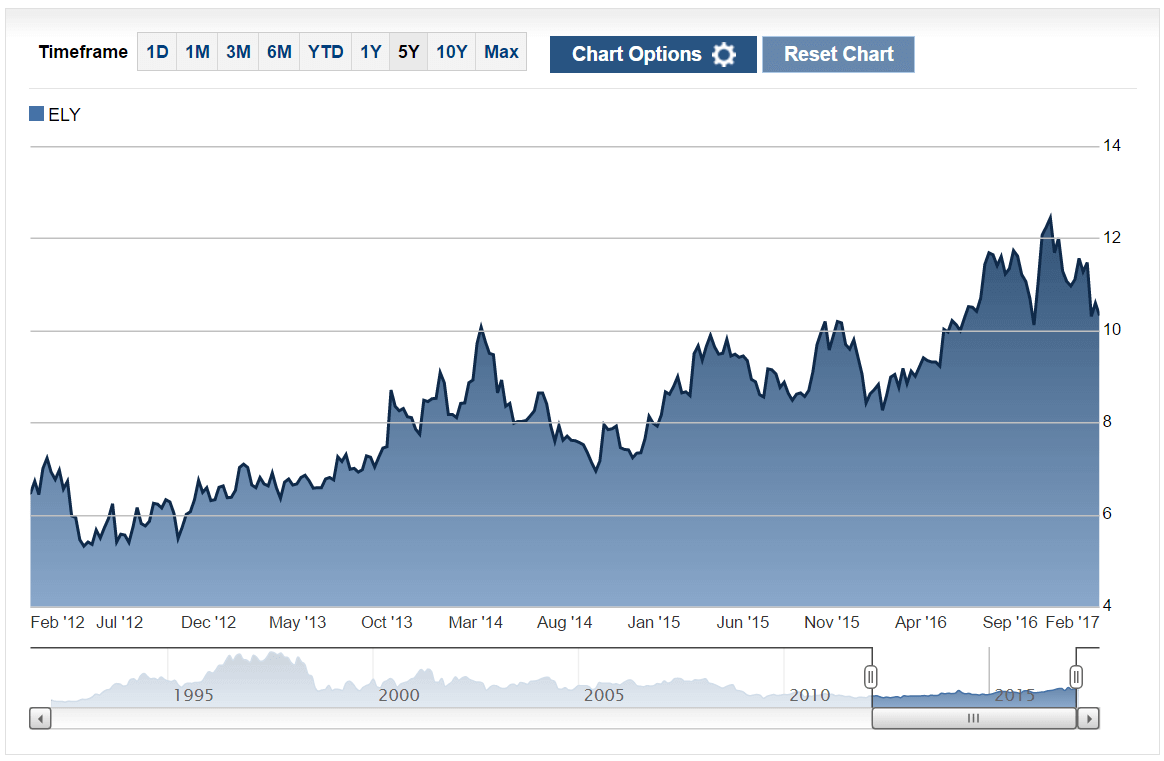

Callaway just released its 2016 full year and 4th quarter earnings report. As you might imagine, Chip Brewer is focusing on the positive. Callaway’s gross revenue is up 7%, and of all the publicly traded golf companies in the world, Callaway has the most cause for optimism. At just over $10 per share, Brewer feels the stock is undervalued, not because of metrics, but because of general unease and unfounded negativity toward golf in general. The stock market, for all of its quantitative analysis, does have a psychological component to it. How consumers feel about a company or product can impact stock price.

There are, however, plenty of positives from which Brewer can draw. In a tough year, Callaway increased market share in the US, Europe and Asia. It grew at a constant currency rate of 2% and its hard goods market share in Asia reached 15.7%. This combined with Callaway’s joint apparel venture in Japan suggests Callaway sees Asia as a source for growth in 2017. From a golf standpoint, there’s plenty of reason to be optimistic.

On the other hand, some analysts feel the stock price isn’t supported by current earnings, and while Callaway is gaining market share, the overall pie isn’t getting any bigger. In fact, it may be getting smaller.

Five years ago, Callaway had a laundry list of issues Brewer needed to fix. With the heaviest lifting behind them, within the context of Wall Street, whatever additional gains Callaway makes will likely be marginal. This is why Callaway’s purchase of Ogio International for $75.5 million in cash makes total sense. Only 38% of Ogio’s revenue in 2015 came from golf related products, and with Ogio’s 2017 total revenue projections at $45 million, Callaway opens two doors. The first gives Callaway the potential to cut existing costs with increased control over its soft goods and golf accessories (bags, apparel, footwear), while the second broaches new territory – lifestyle products such as luggage, totes, backpacks and fitness apparel, which tends to have higher margins.

The increase in total revenue plays well to the casual golf fan, but the scrutinizing investor sees limited upside on a potentially undervalued stock that likely needs a major change in the entire golf landscape if it’s to create anything more than modest single digit growth.

Extended Product Cycles

Don’t trust your eyes. Despite what seems like an onslaught of new product, Callaway has systemically extended the lifecycle of many of its key products. That’s the reality. Nevertheless, some consumers, and even some industry insiders, still believe Callaway is dumping product into the market at an irresponsible and unsustainable rate. Those perceptions have little basis in reality.

The best retailers and consumers can hope for is that prices remain stable until the next generation of product is announced. The EPIC line may be Callaway’s crown jewel, but its release hasn’t impacted the cost of the rest of the Callaway line. While the price of the product it replaces (Great Big Bertha) has dropped, XR16 and XR16 Pro have retained their full retail price.

Since Callaway reestablished what Harry Arnett calls its cadence (its timing, its schedule), there have been no early discounts on anything, and you can be sure the next major Epic release is at least a year away.

Because Callaway has multiple lines within each product category (XR isn’t Epic, Steelhead isn’t Apex) it can effectively stagger its releases. If each sub-line is on an 18-24 month cycle, it may feel like something new is constantly hitting the market, but that’s not exactly the case.

What’s new is, more often than not, categorically different than what came immediately before it. It’s a cadence that has allowed Callaway to maintain price for nearly every product in its lineup. If you drop $500 on the new EPIC, you don’t have to worry that in six months it will be $399 with a free EPIC hat and green lightsaber. That’s not how Callaway does business anymore. Good for them, and good for retailers and all of us too.

The downside of longer product cycles is that they limit short-term revenue, (assuming demand doesn’t increase as a result of an expanding market). It’s unlikely that the average consumer is going to start buying multiple sets of irons or drivers, though I’m sure no OEM would object. So while Callaway may be gaining ground, the steps are small and the market simply isn’t large enough to warrant anything more than very conservative growth estimates.

Callaway may never become a blue-chip stock, because golf equipment may never be a blue-chip industry. Nevertheless, Callaway is poised to become the #1 company in golf. Whether that happens tomorrow, next month or later this year isn’t as important as understanding the new dynamic it creates.

The game requires a different approach when you’re the one with the target on your back, and not every OEM is equipped to handle the attention and scrutiny that comes with being #1 – but Callaway’s different and that’s the point.

CORRECTION: The original version of this story characterized Callaway’s wedge share as #2 and gaining. The most recently available market share data does not support this assessment. We have updated the text accordingly.

B.J. McGee

7 years ago

Great article. Read all the comments. Hit several balls on the range with a friends new Epic driver. Could not believe the feel. Loved it! For me, at 71, feel is everything. Since hitting the Epic, I have sold my Ping G30 driver, two TM rescue woods, and two putters just to save up enough money to buy one.