Golf equipment prices are rising across the board. That’s a fact. Is this increase in price correlated to wage increases and inflation, or is this a byproduct of something else happening in golf?

For those of us that take the game seriously, we’re willing to accept the expense that comes with it. This is a game where degrees and fractions of yards matter and most of us are happy to pay for better-performing equipment that can help us lower scores. But how much is too much? Have we reached a breaking point?

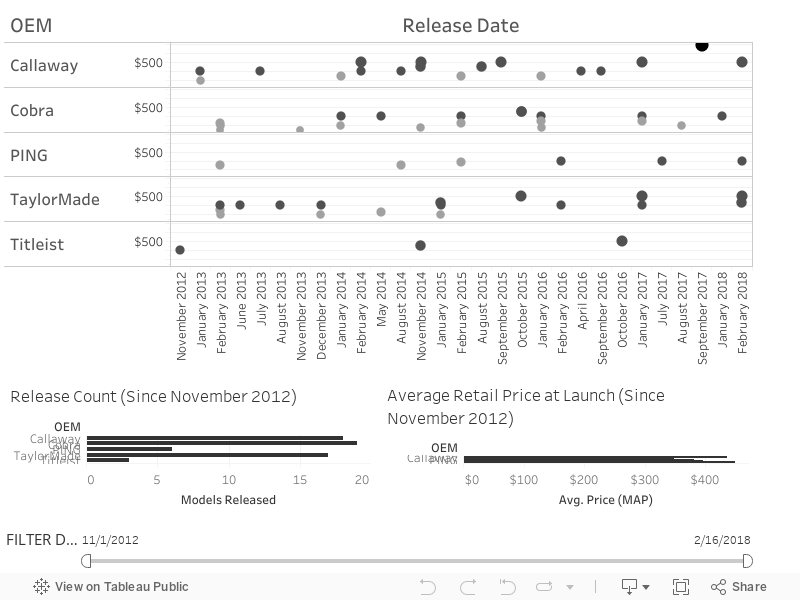

A Look Back In Time

Can we pinpoint the time when prices started to rise appreciably?

To find out, we looked at the cost of mass market drivers from the Top 5 manufacturers in the category beginning in the fall of 2012.

To simplify things a bit, we don’t distinguish between models within the same family, provided the launch date and retail price (at the time of launch) were the same. For example, TaylorMade M3 and M3 440 are treated as one model while the PING G400 Max is differentiated from the rest of the G400 line because of its later release date.

We’ve included only those models that were released through standard retail channels. This means offerings like the Titleist Concept series as well is its MOTO D4 models were excluded. The same is true of big-box exclusives like the legendary TaylorMade SLDR C.

The chart suggests that everybody’s prices have increased since 2013. PING has the most modest increases – up only $50 since 2012. Titleist has steadily increased prices by $50 with each release and now appears comfortable alongside Callaway and TaylorMade with driver prices anchored at $500.

The biggest casualty over this run of increasing prices is the $300 driver. While it wasn’t that long ago that Callaway, TaylorMade, and Cobra offered entry-level drivers for $300, apart from low tech offerings for slower swing speed players, since 2014, the entry point has shifted from $300 to +/-$340, and now to $400. It’s worth noting that with the exception of Cobra’s senior-focused MAX Line, none of the Top-5 manufacturers released a driver with a retail price under $400 in 2018. Among the industry leaders, $400 is entry-level pricing, and there’s less cost differentiation between models.

Why Is This Happening?

To explain the rapid change in pricing, we turned to the OEMs for perspective. Josh Talge, VP of Marketing at Titleist, provided some reasons as to why we’re seeing this increase in price across the industry.

“We ask ourselves this question; How can we make product better each and every cycle? Our 2-year product cycle at Titleist gives us enough time to improve upon the previous product.” – Josh Talge, VP of Marketing at Titleist

Talge provides several reasons why most OEMs are raising prices. Reasons behind the general upward trend at Titleist include:

- Performance seeking each and every cycle (new material research and implementation)

- Using the highest performance partners and suppliers (real deal shafts and grips)

- A different approach to club building and assembly. All Titleist clubs sold in the United States are assembled in Oceanside, CA

- Cost of labor increases over the years

- Time value of money (inflation)

Sound enough reasoning, but have prices really increased that much?

Callaway is quick to point out that the original Great Big Bertha driver launched in 1996 with a retail price of $500. In 2017, the Epic was released for the same price. So in looking at the bigger picture, it’s difficult to definitively say that prices have even kept up with inflation. For example, according to the Bureau of Labor Statistics consumer price index, prices in 2017 are 56% higher than prices in 1996 when Callaway released the Great Big Bertha. That would suggest that $500 in the year 1996 is equivalent in purchasing power to $780.07 in 2017.

“Fish Where the Fish Are”

Cobra’s Tom Olsavsky weighed-in on the comparatively slight increase in Cobra drivers over the years as evidence of the trend.

“Market dynamics have shifted and we may be experiencing more of a market correction. Complex technologies have been added recently to golf equipment, but it’s also important to fish where the fish are.” – Tom Olsavsky, VP of R&D at Cobra Golf

In other words, OEM’s have a greater focus on the serious golfer these days; more so than in the past. The casual golfer just isn’t as invested in the game, so it’s crucial to bring better performing products to the market that the serious golfer will invest in.

While there’s a case to be made that the cost of premium drivers hasn’t changed too much over the last several years, at the lower end of the market has risen in price significantly. Entry-level drivers are drastically more expensive than they’ve ever been before. If we look at TaylorMade for example, it launched two drivers this year (M3 & M4), with price points of $499 and $429, respectively. Back in 2013, TaylorMade released the RBZ Stage 2 driver at a street price of $300. For the industry leaders, the $300 entry-level price point has completely exited the marketplace. Consider Cobra Golf, where entry-level pricing for everything other than its MAX line has climbed from $299 to $329 to$349, and now to $399.

Rob Rigg, who founded popular shoe brand TRUE Linkswear spending time at TaylorMade, says the decision to raise prices came from golfer insights. “OEMs had a desire to price at $300 to satisfy strategic accounts,” said Rigg, “but insights showed that, out of the gate, it’s easier to take money from early adopters/core golfers who pay-up for new tech. Then, discount/cascade later and maintain margin.”

“It was a monumental decision at the time, pushing back against years of ‘wisdom’ as to correct price points, but the writing was on the wall. 15% of golfers spend something like 85% of the money on equipment.” – Rob Rigg

Chalk it up to fishing where the fish are (and higher margins necessitated by participation declines). The industry-wide consensus is that the market is dominated by the serious golfer. It’s a trend that allows bigger OEMs to skip that entry-level market almost entirely. Beginners and recreational golfers will seek out alternatives. For example, they can purchase last year’s model at a reduced price point or buy used, while the core golfer is more willing to spend on the latest and greatest.

The PXG Effect

While some have questioned the long-term viability of PXG’s low volume, high margin model, the company has carved an ever-expanding niche for itself within the industry. Thus far, the company has proven its detractors wrong.

Has PXG incursion into the market influenced industry-wide pricing strategies?

The PXG 0811X driver retails at a whopping $850. That’s a $350 increase over a new TaylorMade M3, Callaway Rogue or Titleist 917D2/D3. PXG has stated that it’s in a market of its own; a position largely supported by price.

Can mainstream brands find their place in a market where $300 or more per iron and $800+ drivers are viewed as reasonable offerings?

In April of 2016, Titleist released its Concept line consisting of the C16 Driver and C16 Irons. The 1,500 drivers produced sold out at $999/each. The 1,500 iron sets, priced at $2,700, also sold out. This is particularly impressive given that the Concept line was never released to the tour and had consequently, exerted little to any influence on sales. C16 exceed expectations to such a degree that Titleist decided to re-release the line in 2017 through a network of fitting centers.

In 2017, Callaway came to market with Epic irons priced at $2,000 per set (3-PW) and a $700 Epic Star driver designed for slower swing speed golfers. Positing itself as a premium brand, both offerings can be viewed as test cases for the ultra-premium market. No doubt it won’t be last time Callaway attempts to penetrate the ultra-premium space?

It’s fair to wonder if either C16 or the Epic Iron exists without PXG.

The Bottom Line

The bottom line is that the cost of golf equipment has increased over the past five years, and it’s unlikely we’ve seen the ceiling. Expectations within the industry are that while prices may remain stable for the next couple of years, further increases are inevitable – and that’s before we consider the possible impact of the recently imposed tariffs. The jump in prices is the result of both increased costs (R&D and manufacturing) and the changing demographics of the game. $500 is the new normal, and $300 – at least among the industry leaders – is a fast-fading memory.

Do the trends concern you or do you see the increases as the reasonable cost of participation in this great game?

Charles Swallow

7 years ago

Mr. Kelly

Well written article, I cited your works in my MBA Marketing class. Nice work, thanks!

I will say that as an avid, I have been willing to adapt to price increase. Looking at the chart, I have had every Titleist driver, and didn’t even realize they have been the most expensive for years! (other than PXG)

Thanks again

CS